The Cypriot economy remains dominated by the attraction and utilisation of external capital. In recent years, the economy has been transforming so that rather than being dependent on a few sectors such as trade, agriculture, tourism and the public sector, it has added sectors such as technology, financial services, professional services and others as a critical means of diversification.

In 2023, the reliance on external capital and Cyprus’ status as a safe haven for investors and refugees saw its greatest expression of success. The previous year, post-COVID recovery spending and the war in Ukraine led to a dramatic influx of funds, companies and individuals relocating to Cyprus. In 2023, this trend continued, driven by the relocation of technology and financial enterprises.

The impact of this inward investment is obvious beneficial for the economy as a whole. But, there are obviously signs that the economy is overheating. Inflation, energy and property prices have increased far beyond a “normal” level, while salaries have lagged far behind. This, in turn, places pressure on both employers as well as employees. This process has also been distorted by the impact of government spending and the attempts of the new President to buy social peace in the public sector through multiple salary raises.

The general effect on Cyprus should be clear: while Cyprus has been known for years as a low-tax, low-cost jurisdiction, for most enterprises and employees today it is a medium-tax, medium- to high-cost jurisdiction. This in turn casts new light on the inability of the government to offer high quality services across multiple sectors of the economy, but most notably in competitive energy production, education, healthcare, municipal services and a rapid and fair justice system.

This article provides a summary forecast of the main macroeconomic indicators for 2024 and what these mean for the wider business model of the island.

GDP and Inflation

Absent a material risk, the Cypriot economy will continue its recovery in 2024. The main drivers of the economy are expected to be service exports, including tourism, professional services, information technology and services, financial services, education, and a few smaller sectors such as agrifood.

The forecasts below should be read taking into account potential exogenous events. These include the absence of a major population surge brought about by a geopolitical conflict as well as energy (oil) prices trading within a band likely characterized by about $70/bbl.

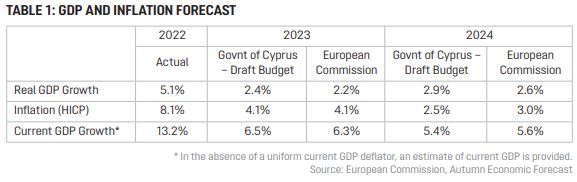

Table 1 clearly indicates the impact of the highly inflationary environment of 2022, when GDP growth was recorded at 5.1% and HICP at 8.1% (based on European Commission figures). The GDP rebound after COVID is due almost entirely to higher public spending, as well as the rebound statistical effect of growth after 2 years of lockdown. Inflation was also high for various reasons: one main one was the influx of over 30,000 Ukrainian refugees into Cyprus, as well as the deferred impact of the “container squeeze”, which touched off significant inflation for a country that depends almost entirely on merchandise imports by seaborne containers.

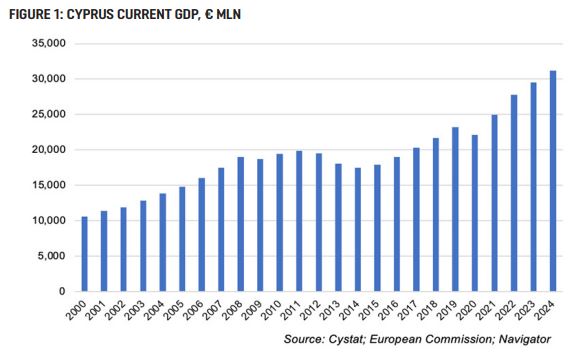

The high but receding inflation predictions for 2023 and 2024 flatter any economic performance that is based on current GDP. If we take the EC forecasts for these three years, Cyprus GDP will have grown by a total of 25.1% over three years, well above its historical average between 2000 and today. This is illustrated clearly in Figure 1, below.

Our estimation of current GDP depends heavily on how inflation is measured. The seriousness of this issue cannot be understated, but a brief assessment is provided in the following section.

Real Inflation Impact

Inflation is measured by the Central Bank of Cyprus based on a methodology agreed upon by all EU member states. This includes a basket of goods and services that is intended to represent an average necessary standard of living. There is much data in Cyprus that leads to the assumption that the real inflation rate for enterprises and most employees in Cyprus is far higher than what is reported.

For example, certain public goods taken for granted in other EU Member States, such as efficient public transport, efficient public education or efficient energy markets, do not exist in Cyprus. This leads to a situation where average companies or employees are forced to double-pay for services that should be provided for by the state.

Moreover, the concept of free and functioning markets in Cyprus may not exist. Successive governments of Cyprus have allowed the build-up of monopolies in multiple areas of the market, ranging from inter-city bus services to airport management to energy production and distribution. As such, neither competition nor innovation can play a normal role in many sectors.

This extends most clearly to property, where rentors have frequently been confronted by increases in annual rent between 7-15%, and by increases in EAC energy prices which this summer doubled in many cases. Even something as basic as legally-controlled rental increases linked to inflation are impossible to effectively control in Cyprus, given the complexity of the 1983 Rent Control Law and the differences between statutory and contractual tenancy.

The result of pricing practices, anti-monopoly and anti-competition enforcement practices in Cyprus is a situation where real inflation observed in the market is far higher than the legally-established inflation based on a basket of goods and services that is probably not fit for purpose to the Cypriot economy.

This has obvious benefits for property owners, the government and employers, and obvious disadvantages for employees (who are also consumers). By keeping legally-recorded inflation artificially low, any cost of living increases for labour can be suppressed.

Let’s also reflect on the absurdity of tax policy. A rising inflation rate lifts prices. Given that the government levies Value Added Tax at the higher rate of 19% on basic goods like energy, education and other staples, this further reduces the disposable income of middle class and lower class consumers. It is a perpetual wonder why the government charges 19% VAT on every electricity bill, given that the energy market remains a government monopoly. This may be necessary to maintain government operations, but it does very little to maintain the living wages of average citizens.

The end result is a situation where a middle class income level finds itself losing approximately 7-10% of purchasing power every year in recent years, while a working class income level faces bankruptcy.

It also means that any enterprise not able to pass on a minimum of 5% high cost base every year to its customers will find itself losing profitability by an equivalent rate.

Minimum Wage versus Living Wage

The pernicious effects of rising inflation and rising costs, and the “blind eye” turned by public authorities on the domestic tax system, are clearly illustrated by the difference between a minimum wage and a living wage.

A minimum wage was established taking effect in Cyprus on 1 January 2023. The minimum wage has been established at €940 per month, of which the first six months of employment are at €885.

Let’s look at the difference between the minimum wage and a living wage for a young, single professional who graduates from university and starts his/her career, living by themselves.

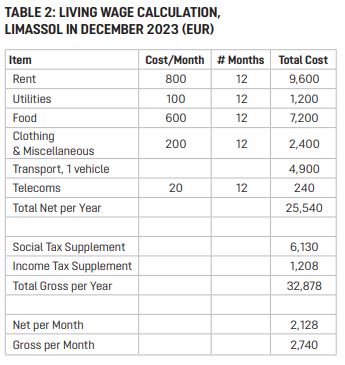

Taking extremely conservative assumptions into account, we assume that a minimum living wage for Limassol, assuming single occupancy rent and utilities, very limited food, and an own car, would cost a net of €25,540 per year.

(The car calculation includes an annual €2,000 depreciation for the vehicle; €50 of fuel per week; €300 insurance. There are no costs for maintenance and repair.)

Because this needs to be a net income, we need to calculate the employer and employee cost of social insurance as well as the employee cost of income tax. This is approximately €6,130 per year in combined social insurance (this calculation is not entirely accurate and includes some assumptions) as well as €1,208 in income tax.

The total gross wage per year is €32,878, or €2,740 per month.

Please compare €2,740 per month legal living wage to the €950 minimum wage.

The difference is absurd. It is not a small rounding error: it is a major and deliberate miscalculation of a living wage. This same magnitude of miscalculation takes place in Paris, London, Brussels and other countries, where it is driving poverty extremism and political polarization. It is hard to argue that the same effects are not taking place in Cyprus.

This lack of a living wage, in turn, is clearly due to a number of structural factors in the economy and in employment:

• There are too many small enterprises in Cyprus, leading to an oversaturation of services and no healthy pricing barriers to competition.

• When employing a young graduate, an employer will quickly understand that the productivity and motivation of this graduate are nowhere near the level required to actually work productively, covering the wage level.

As such, Cyprus is caught in a Fauvian circle of low human productivity, high pricing competition, and rising prices due to the long-term investment policy of attracting foreign investors to Cyprus.

Interest Rates

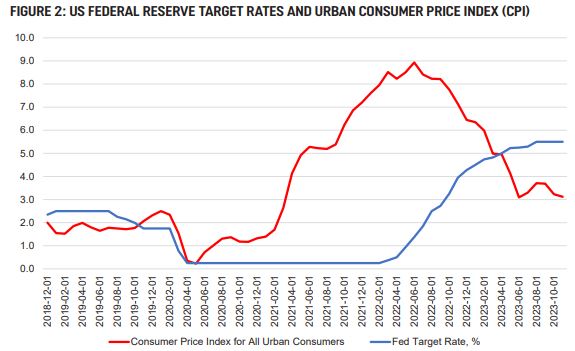

Figure 2 clearly shows the impact of rising interest rates after the March 2020 COVID outbreak in the United States. From a relative low of 0.25% in May 2020, CPI began to rise strongly, ostensibly due to factors such as Chinese Port Closures, the “container squeeze” and an excess of federal support for COVID. CPI reached an annualized high of 8.9% in June 2022, whereupon it began to fall. Today, US CPI hovers around 3% in an economy characterized by full employment.

The US Federal Reserve target rate, in contrast, was lowered to 0.25% in May 2020 in an effort to provide an economic stimulus. A policy debate about the severity of inflation followed, whereupon the Fed began raising rates in March 2022. The US Federal Reserve target rate has been at 5.5% since September 2023, a fact which is causing tremendous financial pain among residential and commercial property borrowers who have seen their variable rate mortgages increase dramatically.

Why is this relevant? The US economy is now functioning at approximately full employment: The US Bureau of Labor Statistics reported a November 2023 unemployment rate of 3.7%, which is a historic low. In this environment, the Federal Reserve will be seeking signs of the economy overheating, i.e. through higher inflation. Should these signs be avoided, then hopefully interest rates will begin to decline in mid-2024, which is also the Federal election year in the United States. This willingness to reduce rates by 0.75 basis points was signalled in a press conference by US Federal Reserve Chairman Jay Powell on 14 December 2023.

Should US interest rates begin to fall, then it is highly likely that the European Central Bank will follow suit. Lower interest rates in the Cypriot context should spark a potential higher demand-driven consumption as debt service costs fall.

Other Sectors

Other key indicators and segments in the Cyprus economy are all pointing to strong performance in 2024. The latest Labour Force Survey shows that the Cyprus workforce has risen to some 494,622 workers in Q3 2023, up from 393,093 workers in Q1 2000, an increase of 56%.

Unemployment has fallen to 5.7% in Q3 2023. The number of vacant jobs in Cyprus reached 12,274, or 2.9% of the labour force in Q3 2023, up by 3,100 vacancies over Q3 2022.

Tourist arrivals from January to October 2023 at up 21.1% over the equivalent amount in 2022. Full year arrivals are likely to reach 3.87 million for 2023, compared to 3.20 mln in 2022. This is very close to the 2019 record of 3.98 mln incoming tourists.

Property prices have continued to rise in 2023. In Q2, the national index of residential property (sales transactions) rose by 7.4% year-on-year. This is split between the house index, which rose by 5.6%, and the apartment index, which rose by 10.1%.

In 2024, we expect a further tightening of the labour force as demand for skilled labour increases. Absent a further geopolitical crisis, tourism should continue to grow by at least 10-12% in volume terms. Property prices will no doubt increase by the same rate as 2023. Although the Build to Rent scheme has been passed, we do not expect tangible results from this within the next 2 years, i.e. to end 2025.

Conclusions

The year 2024 thus presents continuation over the economic performance seen in 2023. While official inflation is set to fall, real inflation will no doubt continue to rise, especially if there is an oil price shock due to a widening of the Israel / Gaza conflict to affect oil tanker traffic in the Persian Gulf, Straits of Hormuz and Red Sea.

The war in Gaza looks set to continue well into the new year, with no tangible solutions in sight. With each passing week, the risk of a greater regional conflagration involving Hezbollah, Syria and Iran increases.

The war in Ukraine will enter its third year in February 2024. Although a recent paralysis appears to be in place, the fighting going on along the entire line of contact is intense.

In November 2024, presidential elections will be held in the United States, and the likely candidates will be Joseph Biden (Democrat) competing against Donald Trump (Republican).

The impact of high interest rates and overinvestment in property and other asset classes is not yet over. It is possible that 2024 will see further failures and liquidation of commercial property firms and other leading borrowers, particularly in the United States. The costs of issuing new debt or rolling over old debt will definitely increase given the 5.5% Fed rate and nearly-equivalent high rates in Europe.

China is also affected by an economic slowdown, driven by high costs, overcapacity, a property crash, and the increasing intensification of control by the Communist Party.

This year, 2024, is also likely to be one of the last years in which a potential solution to the “Cyprus problem” can be sought. Occupied Cyprus is witnessing a building and investment boom as Russians and other migrants settle there. Although inflation and the unsteady value of the Turkish lira is definitely creating financial volatility, the scale of investments is accelerating significantly.

Key priorities for employers in Cyprus must be business model innovation and productivity investments designed to improve operations as well as raise revenue. The impact of continually rising prices and taxes on consumers and employees should not be underestimated. While headline macroeconomic performance will look satisfactory in 2024, this will conceal significant consumer pain which may, in 2025, result in further extremism and volatility in the Parliamentary elections.

Philip Ammerman

Investment Advisor & Angel Investor

Navigator Consulting & Innovation Partners Ltd.