Blockchain-enabled business models will present a seismic shift to how business is conducted in the future. Its impact on commerce will be gamechanging, especially given the increasingly digital global economy and the decentralisation of business models and stakeholders enabled by blockchain. In this direction, a new dimension of innovation awaits.

Everyone should know these 13 things about blockchains

1. Bitcoin, a money exchange system, pioneered blockchain technology and today, it has more than 8 million accounts and grew by more than 100% per year since it began in 2010.

2. Blockchains can be public (like the internet) or private (like an intranet).

3. In terms of its development, blockchain is where the internet was 20 years ago.

4. Only 0.5% of the world’s population is using blockchain today, but 50% or 3.77 billion people use the internet.

5. There is significant investment by today’s tech giants such as IBM and Microsoft in blockchain technology. IBM dedicates $200 million and 1,000 employees to blockchain-powered projects. The average investment in blockchain projects is $1 million.

6. Over the last five years, VCs have invested more than $1 billion into blockchain companies.

7. 90% of major North American and European banks are exploring blockchain solutions. EVERYONE SHOULD KNOW THESE 13 THINGS ABOUT BLOCKCHAINS Bernard Marr, www.forbes.com

8. Blockchains are highly transparent, because anyone with access to a blockchain can view the entire chain.

9. Similar to a Google doc, all participants within a network see all changes to the ledger. The ledger is constantly updated and each participant has their own copy of it.

10. A blockchain is most vulnerable to a breach when it first come online.

11. 9 out of 10 agree that blockchain will disrupt the banking and financial industry. It is estimated that banks could save $8-12 billion annually if they used blockchain technology.

12. One-third of C-level executives are considering adopting or are using blockchain technology.

13. Just like with the internet, there will be jobs that become obsolete. But, there will be new careers that we haven’t even dreamed up yet that will be created as a result of the blockchain transformation.

Bernard Marr, www.forbes.com

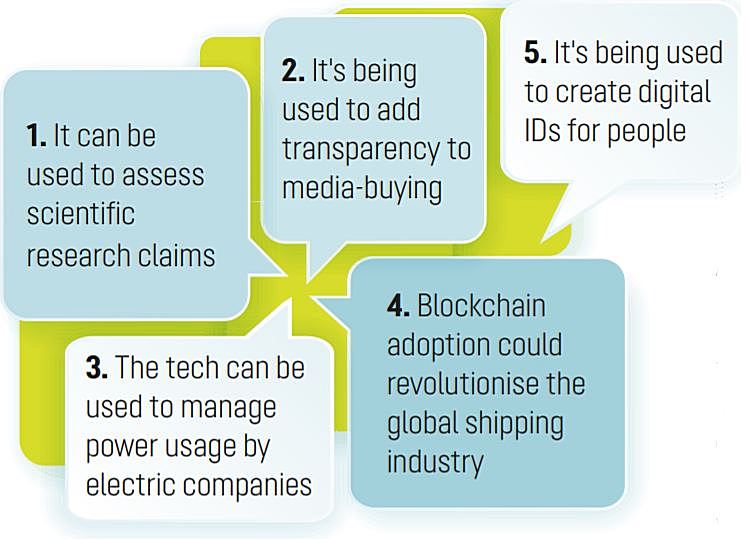

Some ways to use blockchain technologies

Chris Neiger, The Motley Fool

Five reasons that show blockchain is the future

Built on blockchain, cryptocurrencies are decentralised and use a distributed ledger to track, control, and monitor the flow of the transactions. This eliminates central banks, governments and gives control to the users — at least the ones that know what they are doing. But it’s not just fintech; blockchain can also eliminate the game of middlemen in several key areas to bring efficiency, transparency and eliminate corruption at the highest level.

No more middlemen

Diverse implementation potential

Rapid growth in market value

Use in e-governance

Confidence of business leaders.

Suprita Anupam, www.inc42.com

History of blockchain

Cryptographer David Chaum first proposed a blockchain-like protocol in his 1982 dissertation "Computer Systems Established, Maintained, and Trusted by Mutually Suspicious Groups." Further work on a cryptographically secured chain of blocks was described in 1991 by Stuart Haber and W. Scott Stornetta. They wanted to implement a system where document timestamps could not be tampered with. In 1992, Haber, Stornetta, and Dave Bayer incorporated Merkle trees to the design, which improved its efficiency by allowing several document certificates to be collected into one block.

The first blockchain was conceptualised by a person (or group of people) known as Satoshi Nakamoto in 2008. Nakamoto improved the design in an important way using a Hashcashlike method to timestamp blocks without requiring them to be signed by a trusted party and introducing a difficulty parameter to stabilise rate with which blocks are added to the chain. The design was implemented the following year by Nakamoto as a core component of the cryptocurrency bitcoin, where it serves as the public ledger for all transactions on the network.

In August 2014, the bitcoin blockchain file size, containing records of all transactions that have occurred on the network, reached 20 GB (gigabytes). In January 2015, the size had grown to almost 30 GB, and from January 2016 to January 2017, the bitcoin blockchain grew from 50 GB to 100 GB in size. The ledger size had exceeded 200 GB by early 2020. The words block and chain were used separately in Satoshi Nakamoto's original paper, but were eventually popularised as a single word, blockchain, by 2016.

According to Accenture, an application of the diffusion of innovations theory suggests that blockchains attained a 13.5% adoption rate within financial services in 2016, therefore reaching the early adopters phase. Industry trade groups joined to create the Global Blockchain Forum in 2016, an initiative of the Chamber of Digital Commerce.

In May 2018, Gartner found that only 1% of CIOs indicated any kind of blockchain adoption within their organisations, and only 8% of CIOs were in the short-term "planning or [looking at] active experimentation with blockchain".

Source: Wikipedia.org